Why There Are Actually Only 150 Investable Companies

Out of roughly 58,000 publicly quoted shares in the OECD, barely a few dozen—or at most one-to-two hundred if you cast the net worldwide—qualify as true “quality-growth” royalty.

If we start with 58,000 listed companies in the OECD and apply to two filter screens:

Sector & ESG triage. Half the market fails immediately (e.g., oil majors, tobacco) because their business models fail long-term sustainability tests.

Ten Golden Rules filter. From the survivors we applies ten qualitative hurdles (see next section). The result? “No more than five or six dozen companies”—roughly 0.1 % of the starting universe—make the cut at any point in time.

That’s the tiny club this article spotlights.

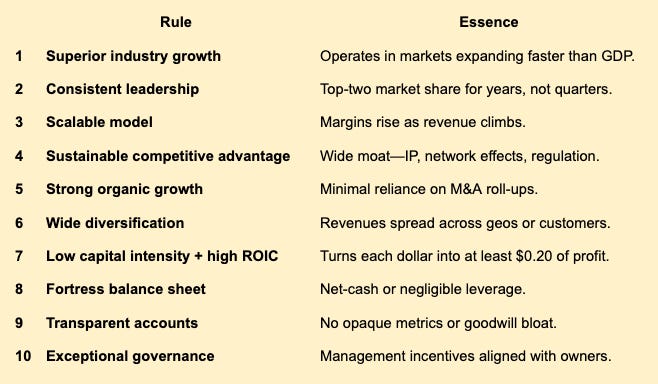

Inside the Ten Golden Rules

These rules operate as a Boolean gate: miss one, you’re out.

How the Universe Shrinks

Sector Exclusions

The initial triage drops entire industries:

Commodities & Extraction – fail Rules 1, 7 (cyclical, capital-hungry).

Banks & Insurers – opaque leverage violates Rule 9.

Telecom Carriers – quasi-utilities with low ROIC.

Autos & Airlines – brutal margins, capital intensity.

That cull alone removes ~30 % of global market cap.

Rule-by-Rule Attrition

Among the 29,000 or so names left, Rule 8 (balance-sheet strength) is the biggest killer—especially after years of cheap debt. Rule 4 (moat) and Rule 9 (accounting clarity) wipe out fast-growing tech names with dazzling top lines but fuzzy cash flow.

Survivors: A Hall of Fame

Recurring alumni include:

Mastercard (Rule 7 poster child, 60 %+ EBIT margin)

ADP (decades-long payroll moat, net cash)

Dassault Systèmes (dominant in 3-D CAD; case study in the book)

Nike (brand moat + pricing power)

Despite different industries, every one ticks all ten boxes simultaneously.

Performance Proof

A concentrated portfolio of 20–25 “only-the-best” names has outperformed the MSCI World by ~1.9 % per year over 27 years, turning $10 k into more than 8× versus 4× for the index—even after three major bear markets. Equally important: volatility is lower, thanks to fortress balance sheets and predictable cash flows.

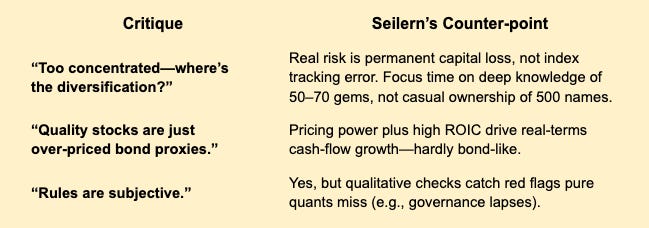

Common Critiques… and Rebuttals

Case Study Snapshot: Why PayPal Was Ejected

Rule 4 breach: Intensifying competition from Apple Pay and BNPL eroded its network advantage.

Rule 8 breach: Share buybacks funded by debt lifted leverage above net-cash comfort.

Outcome: Removed from several quality-growth portfolios in 2023 despite 20 % revenue CAGR—growth ≠ quality.

Looking for the best Monopoly ETFs to invest in?

Check out Monopoly Hunters’ Top Monopoly ETF page on our website to learn about the different monopoly and oligopoly ETFs and what each one has to offer.

Looking for a way to track your investments (in one place)?

Visit Monopoly Hunters’ Free Resources page to download our Ultimate Investment Tracker. It’s free and lets you track all your investments in a single Google Sheet.